What Is a Mining Royalty—and How Much Is Too Much?

Why Royalty Burden Can Make or Break a Project

The Hidden Weight on Every Deposit

In today’s exploration environment, most deposits are no longer “clean.”

They come layered with royalties—NSRs, GRRs, buybacks, sliding scales—that can quietly erode project value long before a mine is ever built.

At first glance, a 2–3% royalty may seem minor. In reality, stacked royalties can be the difference between a buildable project and one that never leaves the ground.

What Is a Mining Royalty?

A mining royalty is a financial interest retained by a third party that entitles them to a percentage of revenue or profit from future production.

Common Types of Royalties

NSR (Net Smelter Return)

The most common. A percentage of revenue after smelting/refining costs.

→ This is what most Nevada projects carry.GRR (Gross Revenue Royalty)

A percentage of total revenue before deductions.

→ More aggressive, less common in hard rock mining.Net Profits Interest (NPI)

Paid after operating costs.

→ Less impactful early, but still reduces upside.Sliding Scale Royalties

Increase with metal prices.

→ Dangerous in bull markets when margins should expand.

Why Royalties Exist

Royalties are often created when:

Property owners retain upside during a sale

Early investors take risk capital

Prospect generators vend projects

Companies defer upfront cash payments

They are, in essence, a way to finance risk with future production.

The Compounding Problem: Stacked Royalties

The real issue is not a single royalty—it’s stacking.

A project might carry:

2% NSR (original owner)

1.5% NSR (option agreement)

1% NSR (strategic investor)

Total: 4.5% NSR

At that level, you are no longer dealing with a minor encumbrance—you are fundamentally altering project economics.

Case Study: Nevada’s Fourmile Project

The Fourmile Project, controlled by Barrick Gold Corporation, is widely regarded as one of the most significant recent gold discoveries in Nevada’s Cortez District.

Geologically, it is a high-grade, structurally controlled gold system hosted in carbonate rocks in the footwall of the Roberts Mountains Thrust. Mineralization occurs in steeply dipping breccia bodies associated with the Sadler fault system and related anticline structures, with a footprint of roughly 2.4 km.

While broadly Carlin-type, Fourmile stands out due to:

Strong silicification

Minimal preg-robbing carbon

Multiple hydrothermal events (silicification, decalcification, argillization, sulfidation)

This results in:

Exceptionally high-grade intercepts, with reported averages in the ~15–16 g/t gold range

Favorable metallurgy relative to typical Carlin systems

Breakdown of the Royalty Stack

Despite its geological strength, Fourmile is encumbered by multiple legacy interests:

1. Teck Resources – Net Profits Interest (NPI)

~10% NPI

Increases to 15% after 6 million ounces produced

Carry-free

Implication:

Barrick funds development entirely while Teck participates in downstream profits—making this the most significant long-term economic burden.

2. Royal Gold – 1.6% GSR

Royal Gold holds a 1.6% Gross Smelter Return

Implication:

Direct reduction to top-line revenue regardless of operating costs.

3. Rio Tinto – ~1.2% Gross Production Royalty

Rio Tinto holds a ~1.2% sliding-scale royalty

Implication:

Royalty increases with gold price, limiting upside in strong markets.

Why This Structure Matters

These royalties operate at different levels of the economic stack:

GSR + gross royalty → reduce revenue immediately

NPI → captures downstream profitability

This creates a layered system where:

Revenue is reduced first

Costs are borne entirely by the operator

Remaining profits are shared

The Real Economic Effect

The issue is not just percentage—it’s interaction.

~2.8%+ removed from revenue (GSR + gross royalty)

Followed by 10–15% of profits

Resulting in:

Lower margins

Reduced NPV and IRR

Longer payback periods

Diminished acquisition appeal

How Much Royalty Is Too Much?.

Industry Benchmarks

1–3% NSR (or equivalent) → Normal / Financeable

Standard range across most viable projects. Typically does not materially hinder development.5–8% Total Royalty Burden → High / Constraining

Begins to noticeably compress margins and limit financing flexibility. Requires strong grades, good metallurgy, and favorable infrastructure.8–10%+ Total Royalty Burden → Often Unsustainable

At this level, projects struggle to generate sufficient returns. Development becomes highly sensitive to commodity prices and cost inflation.

Why These Thresholds Matter

Royalty burden scales directly with revenue—but its impact on value is nonlinear.

1. Margin Compression Accelerates

A move from 2% to 6% is not a 3x problem—it can:

Increase cutoff grades

Reduce recoverable ounces

Shorten mine life

2. Financing Becomes Increasingly Difficult

As total royalty burden rises:

Lenders discount cash flow more aggressively

Majors demand higher returns

Equity dilution increases

3. Sensitivity to Metal Prices Increases

Higher royalties:

Amplify downside risk in weak markets

Cap upside in strong markets (especially with sliding scales)

Important Distinction: Not All Royalties Are Equal

A key nuance—especially relevant to the Fourmile example:

3% NSR alone → manageable

3% GSR + 10% NPI → materially more severe

Royalties that stack across revenue and profit levels compound their impact.

Putting Fourmile in Context

Using these thresholds:

Revenue-level royalties: ~2.8%+

Profit-level royalty: 10–15% NPI

While it doesn’t fall cleanly into a single percentage band, the combined burden clearly pushes into the “high to extreme” category.

And yet, it works—because of:

~15–16 g/t grades

Favorable metallurgy

Tier-1 infrastructure

Which reinforces the broader conclusion:

If a project needs elite geology to withstand its royalty structure, the royalty is already too high for most deposits.

When High Royalties Can Work

High royalty burdens are not automatically disqualifying—but they impose strict requirements on a project.

In practice, only a small percentage of deposits can sustain 5–10%+ total royalty structures and remain economically viable.

1. Exceptional Grade

Grade is the most direct offset to royalty burden.

Higher grade → more revenue per tonne

Greater margin after royalties

Lower sensitivity to cost increases

At Fourmile, reported grades of ~15–16 g/t Au provide a margin profile capable of supporting both:

Revenue-level royalties

Profit-level participation (NPI)

Without strong grade, most high-royalty projects fail early in economic evaluation.

2. Favorable Metallurgy

Metallurgy determines recovery and processing cost.

Projects that can support higher royalties typically have:

High recovery rates

Simple processing flowsheets

Minimal penalty elements

Fourmile benefits from:

Minimal preg-robbing carbon

Strong silicification

Relatively straightforward processing compared to refractory systems

Complex metallurgy combined with high royalties is often prohibitive.

3. Strong Structural Continuity and Scale

A deposit must be both high-grade and laterally consistent.

Key requirements:

Continuous mineralization

Predictable geometry

Expansion potential

Fourmile’s:

~2.4 km mineralized footprint

Structurally controlled high-grade zones

…support the scale required to justify development despite royalty burden.

4. Existing Infrastructure and Processing Synergies

Infrastructure reduces capital intensity and improves project economics.

Projects that can support higher royalties often benefit from:

Nearby processing facilities

Established access and power

Reduced capital expenditures

Fourmile’s location within the Cortez complex provides:

Potential access to existing processing infrastructure

Lower incremental capex

Faster development timelines

Lower capital requirements help offset long-term revenue reductions from royalties.

5. Strong Commodity Price Environment

Higher metal prices can improve project economics:

Increased revenue enhances margins

However, royalties scale with price (especially GSR and sliding-scale structures)

High prices can enable development, but they do not resolve structural royalty burden.

6. Major Operator Advantage

Large operators can support projects that would not be viable for juniors.

Companies such as Barrick Gold Corporation benefit from:

Existing infrastructure

Lower operating costs at scale

Internal processing capacity

Strong balance sheets

A junior company with the same project would face:

Higher capital costs

Greater financing risk

Increased sensitivity to royalty burden

What is viable for a major operator is often not viable for a junior.

The Critical Reality

Even under optimal conditions, high royalties still:

Reduce project NPV

Extend payback periods

Limit operational flexibility

What Investors and Geologists Should Look For

In modern exploration, evaluating a deposit is no longer just about geology—it is about ownership. Royalty structures can materially alter project economics, even in otherwise strong systems. Investors and geologists must look beyond grade and scale to understand how much of a project’s value can realistically be retained.

When evaluating a project:

Key Questions

What is the total royalty burden (not just individual pieces)?

Are there buyback options? At what cost?

Do royalties stack across claims or ownership blocks?

Are there sliding scale triggers?

Red Flags

Total NSR above ~4%

No buyback provisions

Multiple legacy agreements

Poor documentation or unclear ownership

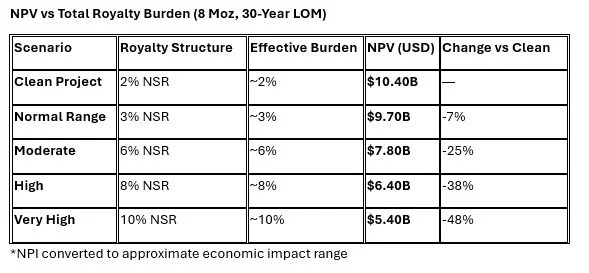

Quantifying the Impact: Royalty Burden vs Project Value

Understanding royalty structure qualitatively is essential—but its real significance becomes clear when measured quantitatively. Even small increases in royalty burden can translate into substantial reductions in project value over time.

The following model applies a range of royalty scenarios to a large-scale, long-life gold deposit to demonstrate how royalty burden impacts Net Present Value (NPV) under realistic operating conditions.

Theoretical Royalty Impact on Project Value (NPV Sensitivity)

Net Present Value (NPV) is the current value of all future cash flows from a project, adjusted for time and risk.

Assumptions (Theoretical Values)

Deposit size: 8 Moz gold

Mine Life: 30 years

Annual Production: ~267,000 oz/year

Gold Price: $4,500/oz

Recovery: 90%

AISC: $1,500/oz

Initial Capex: $1.6B

Discount Rate: 5%

NPV Calculation Methodology

The Net Present Value (NPV) used in this analysis is calculated using the standard discounted cash flow (DCF) model:

NPV = Σ [CFₜ / (1 + r)ᵗ] − C₀

Where:

CFₜ = Cash flow in year t

r = Discount rate (5% in this model)

t = Year of production (1–30)

C₀ = Initial capital expenditure ($1.6B)Annual cash flow is derived from:

Gold price

Production rate

Recovery

AISC

Royalty burden (applied to revenue and/or profit depending on structure)

NPV vs Total Royalty Burden (8 Moz, 30-Year LOM)

These are all theoretical calculations and do not reflect any real companies or projects and is a theoretical equation producing theoretical NPVs

Strategic Takeaway

Modern exploration is not just about finding ounces—it’s about owning them cleanly.

The best projects today are:

Geologically strong

Located in Tier-1 jurisdictions

Minimally encumbered by royalties

Because at the end of the day:

A great deposit with a heavy royalty can be worth less than a good deposit with a clean title.